COVID-19: Federal Reserve Eyeing Launch of Main Street Lending Program in June 2020

The Federal Reserve (Fed) recently announced its expectation that the Main Street Lending Program will finally get off the ground in early June. This long-awaited announcement comes more than two months after the Fed first published its intent to establish a program to facilitate loans to small and mid-size businesses that were in sound financial condition prior to the onset of the COVID-19 pandemic.

The implementation of the Program will provide much needed assistance via available credit to eligible entities that need assistance in recovering from the economic impact caused by the pandemic.

Background

On March 23, 2020, the Fed issued a press release stating its intention to create a lending program to assist businesses experiencing financial strain due to the economic disruptions caused by COVID-19. The Fed announced the creation of the Main Street Lending Program on April 9, 2020 and released the initial term sheets for the Program’s two loan options. On April 30, 2020, the Fed issued updated term sheets, revised the Program, and released guidance in the form of frequently asked questions (FAQs). The revised Program created a third loan option and clarified several key questions and material concerns raised by the more than 2,200 letters the Fed received from the public.

Overview of the Program

The Program, as revised by the Fed’s term sheets and accompanying guidance released on April 30, 2020, consists of three lending facilities: the Main Street New Loan Facility (MSNLF), the Main Street Expanded Loan Facility (MSELF), and the Main Street Priority Loan Facility (MSPLF). All three of the facilities have similar structures and will be funded by the Federal Reserve Bank of Boston (Reserve Bank) through a single common special purpose vehicle (SPV). The Department of Treasury, as authorized by the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), will initially fund the SPV with a $75 billion equity investment. The SPV will purchase either 85% or 95% of participation in the loans received by Eligible Borrowers and originated by Eligible Lenders in any of the twelve Fed districts depending on the loan facility.

Eligible Lenders

Eligible Lenders include federally insured depository institutions (i.e., banks, savings associations and credit unions), US branches or agencies of foreign banks, US savings and loan holding companies, US bank holding companies, and US subsidiaries of the above. Under the Program, Eligible Lenders will sell participation in the loans of either 85% or 95% to the SPV and retain the remaining portion of the loan. Eligible Lenders are required to hold the remaining portion and bear the related risk until the earlier of the maturity of the loan or sale by the SPV of its participation.

Eligible Borrowers

To be classified as an Eligible Borrower under the Program, an entity must be organized for profit as a corporation, limited liability company, partnership, association, trust or cooperative; a joint venture with no more than 49 percent non-US ownership; or a tribal business concern. Also, the entity must: (1) be established prior to March 13, 2020; (2) have either (i) 15,000 or fewer employees (includes all full-time, part-time and temporary employees); or (ii) 2019 annual revenue of $5 billion or less; (3) be organized or created under the laws of the US with significant operations in and a majority of its employees based in the US; (4) not have received support pursuant to Section 4003(b)(1)-(3) of the CARES Act; (5) not be insolvent (all borrowers must certify that they have the ability to meet their financial obligations for at least 90 days and that they do not expect to file for bankruptcy during the same time period); (6) have been in sound financial condition prior to the onset of the COVID-19 pandemic; and (7) not be an ineligible business (as listed in 13 C.F.R. §§ 120.110(b)-(j), (m)-(s)).

Eligible Borrowers may not participate in more than one of the lending facilities under the Program. Additionally, Eligible Borrowers may not participate in both the Program and the Fed’s Primary Market Corporate Credit Facility (PMCCF). However, a business who has received a PPP loan is not precluded from participating in and receiving a loan under the Program. An Eligible Borrower who receives a loan under one of the Program’s lending facilities may receive more than one loan under the same lending facility so long as the aggregate amount received does not exceed the maximum amount allowed under such lending facility.

Eligible Loan Terms

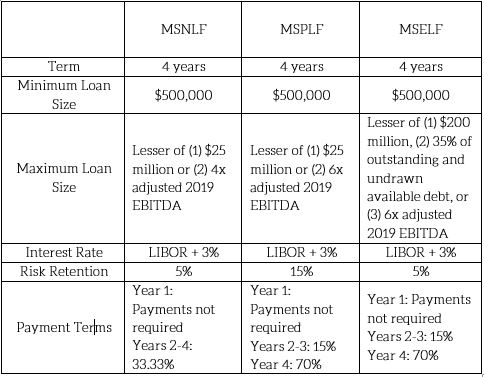

An Eligible Borrower may apply to an Eligible Lender for an Eligible Loan under one of the Program’s three lending facilities: the MSNLF, the MSPLF, or the MSELF. The following chart provides a summary of the key features and terms for Eligible Loans under each of the three loan facilities:

Notably, the Program is different from other COVID-19 related programs such as the PPP in that the loans issued under the Program’s lending facilities are not forgivable.

Borrower Certifications and Restrictions

Importantly, it must also be noted that Eligible Borrowers are required to make certain certifications and adhere to certain restrictions as set forth in the CARES Act when accepting a loan under this Program. While the loan is outstanding, and for the twelve months following full repayment, an Eligible Borrower is restricted from paying dividends on its common stock, or repurchasing its own equity securities or that of its parent company, unless contractually required to do so. Also, Eligible Borrowers are prohibited from using the proceeds of a loan under this Program to voluntarily prepay other loans or reduce other outstanding credit lines unless done in the ordinary course of business, except in the event of a default. Eligible Borrowers may, however, use proceeds from an MSPLF loan to refinance existing debt owed by the Eligible Borrower to a lender other than the Eligible Lender used to procure the loan.

Additionally, Eligible Borrowers must comply with certain compensation restrictions during the same period. Those compensation restrictions include: (1) no increases for employees or officers making more than $425,000 in calendar year 2019, unless employee compensation is determined through an existing collective bargaining agreement; (2) limiting severance upon termination of an employee or officer making more than $425,000 in calendar year 2019 to less than twice the total compensation for that employee or officer in calendar year 2019; and (3) cutting back employees or officers whose total compensation exceeded $3 million in calendar year 2019 to no more than $3 million plus 50% of the employee’s or officer’s total compensation over $3 million in calendar year 2019.

Further, while not required, Eligible Borrowers are encouraged to make commercially reasonable efforts to retain employees during the term of the loan. In particular, Eligible Borrowers are expected to make good-faith efforts to retain employees and maintain payroll in light of the current economic environment, its available resources, and its labor needs. This is important considering interested entities who apply for and receive a loan under this Program will have their name and loan amount released to the general public each month by the Fed.

How to Apply

To obtain a loan under the Program, an interested entity should contact an Eligible Lender to determine the entity’s eligibility. Eligible entities who meet the requirements of the Program shall work together with the Eligible Lender to submit an application to the Eligible Lender with all other documentation required by the Eligible Lender’s underwriting process.