The Rise of Defaults in the Commercial Real Estate Market: How the Uniform Commercial Real Estate Receivership Act Can Protect and Maximize the Value of Lenders’ Security Interests

Mounting financial obligations and the lack of easily accessible cash has turned the U.S. commercial real estate market upside down in recent months. As of late May, an estimated $32 billion worth of commercial property loans were in “special servicing,” double the numbers reported in February. And in April and May, apartment and office properties missed payments on approximately $7.1 billion in mortgages, up from around $4.2 billion in February and March. These increases appear to be just the beginning of a larger trend, with tenants expected to miss rent payments in June and July, causing lenders to brace for sweeping loan defaults.

Indeed, lenders will likely be racing to preserve the value of their collateral through the institution of commercial real estate foreclosure proceedings, resulting in a backlog of cases that may further impair the value of commercial real estate already in substantial decline.

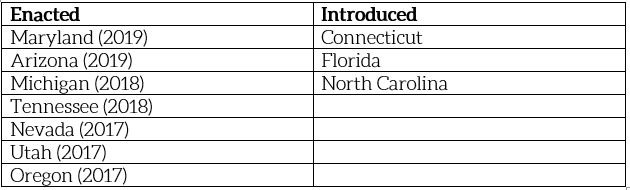

However, in those states fortunate to have enacted, or soon to be enacting, the Uniform Commercial Real Estate Receivership Act (UCRERA), lenders and other interested parties have the benefit of efficient and effective remedies and procedures to protect their interests in commercial property, as well as personal property used to operate and maintain the commercial real property, through the institution of receiverships actions. To date, the following states have either enacted or introduced the UCRERA as law:

The number of states that have enacted the UCRERA is limited, to be sure. However, even if the UCRERA has not been adopted by your relevant jurisdiction, the UCRERA’s rules, with its clear ties to the uniform bankruptcy code, common law, and familiar equitable principles, should not only prove to be helpful guidance, but serve as a persuasive source of precedent for lenders seeking to preserve the value of their collateral pending disposition of the same. Indeed, foreclosure actions have been successfully pursued in non-UCRERA jurisdictions pursuant to court orders seemingly paralleling the UCRERA’s procedures and guidance.

What is a Receivership Action?

Receivership is an equitable remedy allowing a court to oversee the orderly management and disposition of property subject to a lawsuit. A receiver is a person appointed by a court, pursuant to its equitable power, to take possession of the property of another and to “receive, collect, care for, and dispose of the property or the fruits of the property.” 1 Clark on Receivers § 11(a), at 13 (3d ed 1959). Like bankruptcy proceedings, receiverships permit an appointed receiver to efficiently administer commercial real property during the pendency of litigation concerning the property’s disposition resulting from the borrower’s insolvency.

And while receiverships are widely used throughout the United States, there is no standard set of receivership rules such as those present in bankruptcy proceedings. Indeed, courts of different states have applied widely varying standards in conducting state court receiverships, with standards even varying from one county, district, or municipal subdivision to the next within a state, as individual judges might have divergent perspectives on the circumstances giving rise to a receivership and whether those constitute sufficient grounds for the establishment of a receivership.

Receiverships in the Commercial Real Estate Context

One of the biggest issues facing lenders in the commercial real estate market is time. Generally, a lender obtains a lien in real property as security for its loan. A lien is not to be confused with an ownership interest, however, and when a borrower defaults on a loan, the lien itself does not give the lender the right to take immediate possession of the property. Rather, the lender needs to go through the foreclosure process.

However, the foreclosure process raises a host of concerning issues for a lender. The process may take a substantial amount of time depending on the jurisdiction, leaving the real property subject to waste, deterioration, or immediate harm, threatening the value of the lender’s security. Where the property has a high vacancy rate, the lender’s assignment of rents, may have limited-to-no value to the lender.

The lender’s collateral may also include substantial personal property, such as the furnishings and equipment in the case of a hotel or resort, that may be at risk of being removed or damaged upon default. Or there may be reasons, such as existing or ongoing environmental contamination, that a lender may not want to be in the chain of title.

Commercial Real Estate Receiverships under the UCRERA

Courts commonly appoint receivers at the request of a lender that seeks to enforce a mortgage in default. Typically, commercial real estate mortgages or deeds of trusts explicitly provide that upon default, the lender may seek the appointment of a receiver from a court with jurisdiction over the mortgaged premises.

Frequently, the terms of the mortgage or deed of trust purport to provide the lender consent for the appointment of a receiver following default. But even if the loan documents provide for the appointment of a receiver, the loan documents and applicable state law rarely provide guidance as to either the scope of the receiver’s powers or the mechanics of the receivership itself.

A. Appointment of Receiver & Receiver’s Disinterestedness

Under the Act, a receiver is appointed, and thus a receivership estate is created, only after notice and an opportunity for hearing. The Act establishes standards under which a court may appoint a receiver in the exercise of its equitable discretion. The Act also establishes standards under which a petitioning mortgage lienholder is entitled to appointment of a receiver, either as a matter of right or as a matter of the court’s discretion. Where the court appoints a receiver on an ex parte basis, the court may require the party seeking appointment to post security for any damages, attorney’s fees, and costs incurred by a person injured by an appointment later determined to be unjustified.

B. Receiver’s Lien Priority and Control of Property

On appointment, a receiver has the status and priority of a lien creditor with respect to receivership property. Appointment of a receiver does not affect the validity of a pre-receivership security interest in receivership property, and property acquired after appointment is subject to any pre-receivership security agreement to the same extent as if no receiver had been appointed. Similar to the powers of a trustee or debtor-in-possession in bankruptcy, the receiver, upon appointment, has the power to gather property and collect debts that are receivership property.

C. The Act’s Contemplation of a Stay of Other Proceedings

Importantly, and what is often a major chasm between a bankruptcy proceeding and a state receivership proceeding, the Act contemplates an applicable stay of proceedings upon the order of appointment, applicable to all persons, of an act to obtain possession of, exercise control over, or enforce a judgment against receivership property, as well as an act to enforce a lien against receivership property. Like bankruptcy proceedings, the court can expand the scope of the stay, and grant relief from the stay.

D. The Receiver’s Ability to Sell, Lease, License or Transfer Receivership Property Other than in the Ordinary Course

Where some states have limited a receiver’s ability to sell commercial real property, the Act permits the receiver, after court approval, to use, sell, lease, license, exchange or otherwise transfer receivership property other than in the ordinary course of business. Moreover, like Section 363(f) of the Bankruptcy Code, the transfer of property is free and clear of rights of redemption and liens other than liens that are senior to the lien of the person who obtained the receiver’s appointment. Liens extinguished by the receiver’s sale attach to proceeds with the same validity, perfection, and priority as they had with respect to the property sold.

E. Executory Contracts and Unexpired Leases.

F. Organized Claims Process and Transparency

The Act requires the receiver to notify creditors of the appointment of the receiver unless the court orders otherwise, and requires creditors to file claims with the receiver as a precondition to obtaining any distribution from receivership property or the proceeds of such property. The Act permits the receiver to recommend disallowance of claims. The Act also authorizes the court to forgo the filing of unsecured claims where the receivership property is likely to be insufficient to satisfy secured claims against the property.

G. Receivership in Context of Mortgage Enforcement.

The Act makes clear that the appointment of a receiver on request by a mortgagee or assignee of rents, and actions taken by the receiver, do not make the mortgagee or assignee of rents a “mortgagee in possession,” do not constitute an election of remedies or make the secured obligation unenforceable, and do not constitute an “action” within the meaning of a state’s “one action” rule.

Conclusion

And even if a lender’s particular jurisdiction has not formally enacted the UCRERA, the clear framework it provides for conducting a state court receivership is certainly transferable to non-UCRERA jurisdictions. Foreclosure actions, based on similar concepts and procedures to the UCRERA, have been successfully litigated in non-UCRERA jurisdictions.

Bailey Glasser has successfully argued for and received orders substantially in-line with the rules, guidance, and procedure of the UCRERA in non-UCRERA jurisdictions.